If you have trouble viewing this email, please click here.

If you have trouble viewing this email, please click here. |

|

| The Brode Report | April 2017 | Uber Teardown

|

|

I created a short video where I describe some unique features of a financial model that I developed for a client that raised over $350 million. You can see it at brodetelecom.com/model-overview. |

|

I’ve had negative views about companies before. Back in 2011-2012 I thought Groupon was trading at ridiculous prices and wrote a series of newsletters about that. You can see them here, here, here, here, here, here, and here. Bottom line, Groupon had a chance to sell to Google in 2010 for $6 billion, but went with an IPO and a $16B valuation. Since then, the stock has tanked. Current market cap is $2B. Oh, and Google/Alphabet is up 350% since 2010, so that $6B would be worth over $20B. Clearly Groupon should have bought the deal!

So now it’s time to look at the biggest unicorn of them all: Uber. The good news Uber reported in 2016 was that it seemed to turn a corner in profitability, with the company moving, at long last, towards profitability.

Source: Naked Capitalism, piece #1 of 4, which did a great job pulling together financials from various sources. Note that 2H15 is missing; Uber didn’t report results for Q415. However, there are three problems here:

So if Uber needed to be profitable now, it seems the only lever they have is to change the percentage of gross passenger payments that they take. In 1H16 Uber would have needed another 15% of gross payments just to hit break even, taking their share to 38%. And if they had a margin similar to, say, Google’s 25% of revenue? Then they’d need 50% of gross revenues. If you think drivers can’t make it now on ~80% of the revenue, how will they do with 50%, a 37% pay cut? Can Uber grow their way out of this problem? Some suggest that Uber’s market is not the taxi market but something much larger:

That quote is from The Economist. I like how they tell us that Morgan Stanley is a bank. :-) Let’s explore this by following the methodology of Professor Aswath Damodaran, laid out in a 538 article back in 2014. To summarize, he calculated Uber’s valuation using a combination of market size, market share, and % of gross collections kept by Uber. Further, and crucially, he assumed a 40% EBITDA margin. In his base case, even with a 10-year forecast, the discounted terminal value was still 80% of the NPV. Damodaran used market sizes ranging from $50-300 billion and came up with values of $3-18 billion at a 10% market share. So with a $10 trillion market (10,000 billion), could Uber get 100x Damodaran’s valuation ($5.9B valuation at a $100 billion market) and thus be worth $590 billion and thus have upside from their current $60 billion valuation? I doubt it, and start with these reasons:

At this point, I’d expect Uber to face valuation pressures in the near term. This unicorn may turn out to be a mythical creature after all. |

|

|

The Brode Group |

Strategic Financial Consulting - Real-World Results |

(303) 444-3300 |

Hi,

Hi, By contrast, my

By contrast, my

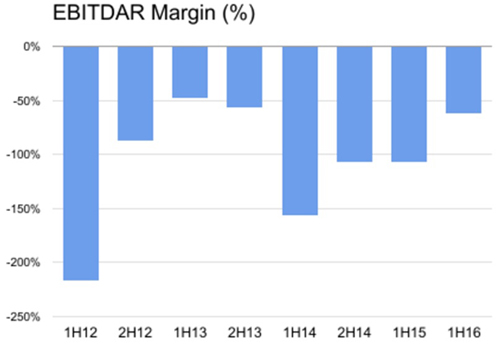

Um, how about the whole concept of EBITDAR in the first place? I accept EBITDA as a useful measure, essentially “operating profit without noncash items.” My antennae start to go up when companies add more letters onto the acronym so they can exclude more costs. I

Um, how about the whole concept of EBITDAR in the first place? I accept EBITDA as a useful measure, essentially “operating profit without noncash items.” My antennae start to go up when companies add more letters onto the acronym so they can exclude more costs. I  Finally, I feel the need to address the hype around self-driving cars as the ultimate endgame for Uber. First, this wasn’t part of the original story, so I’m a bit skeptical that this isn’t just hype to get us to lose focus from the fact that the original business model hasn’t panned out. Second, I find it hard to believe that Uber is the best-positioned company to take advantage of a driverless car world. Why wouldn’t Ford have an advantage in procuring vehicles cheaply? Anyone can build an app. Google can aggregate traffic. Finally, it seems like there might be shenanigans in the self-driving car side of Uber, as recent news reports have raised. While this has been covered in large national outlets, I found

Finally, I feel the need to address the hype around self-driving cars as the ultimate endgame for Uber. First, this wasn’t part of the original story, so I’m a bit skeptical that this isn’t just hype to get us to lose focus from the fact that the original business model hasn’t panned out. Second, I find it hard to believe that Uber is the best-positioned company to take advantage of a driverless car world. Why wouldn’t Ford have an advantage in procuring vehicles cheaply? Anyone can build an app. Google can aggregate traffic. Finally, it seems like there might be shenanigans in the self-driving car side of Uber, as recent news reports have raised. While this has been covered in large national outlets, I found